A Final Update on Q4 Earnings

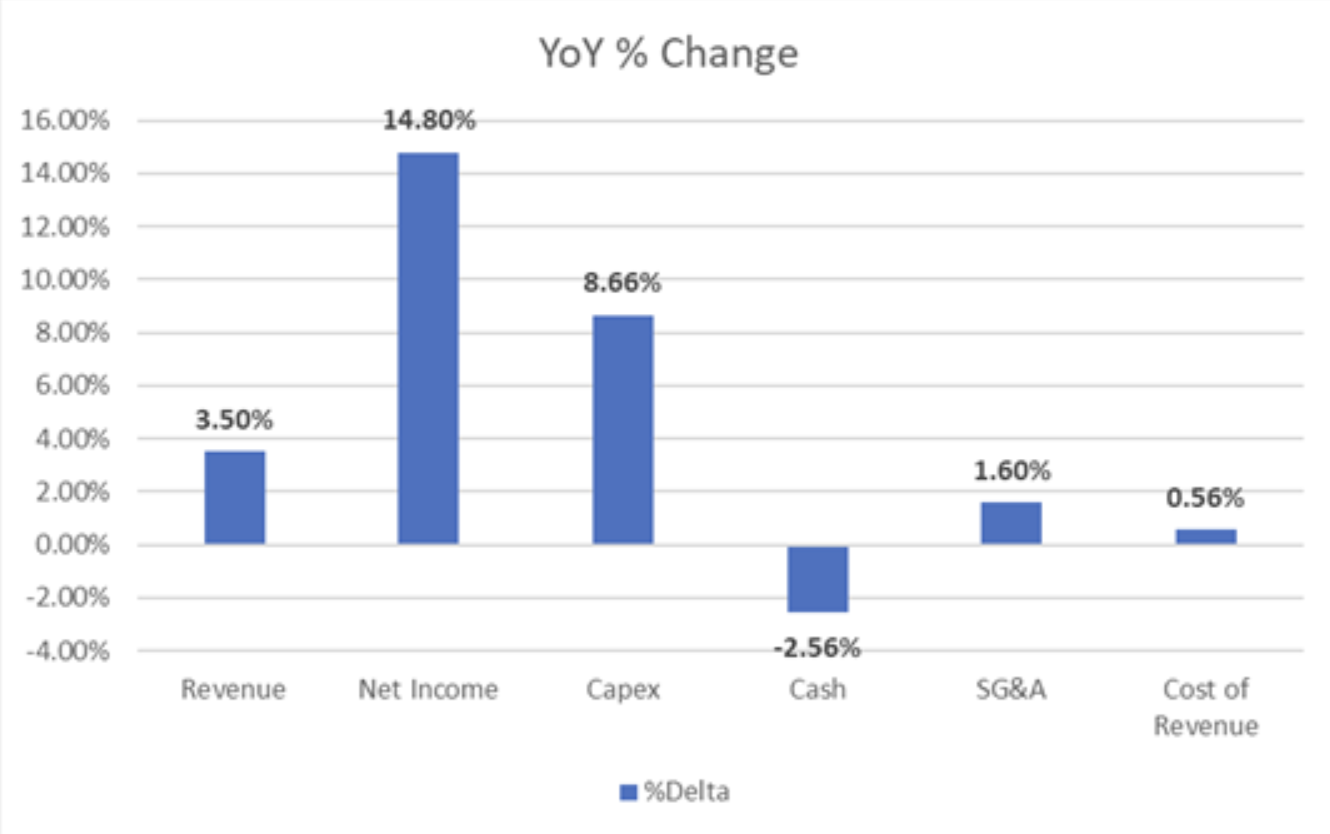

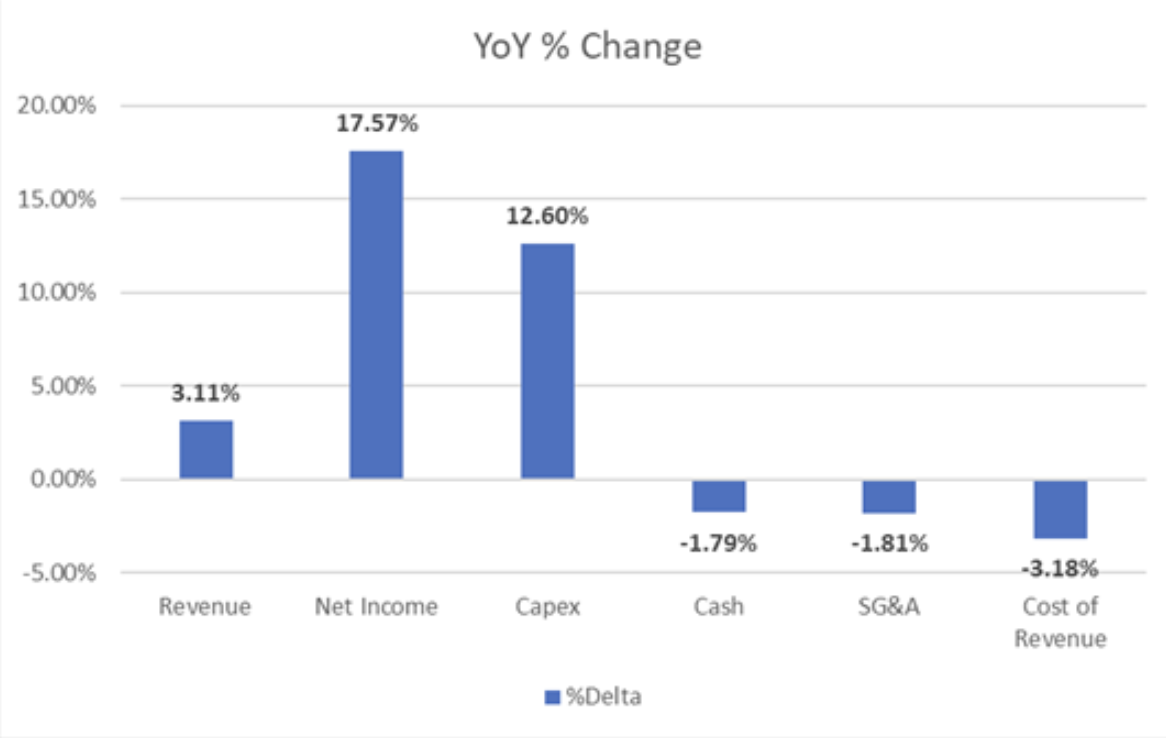

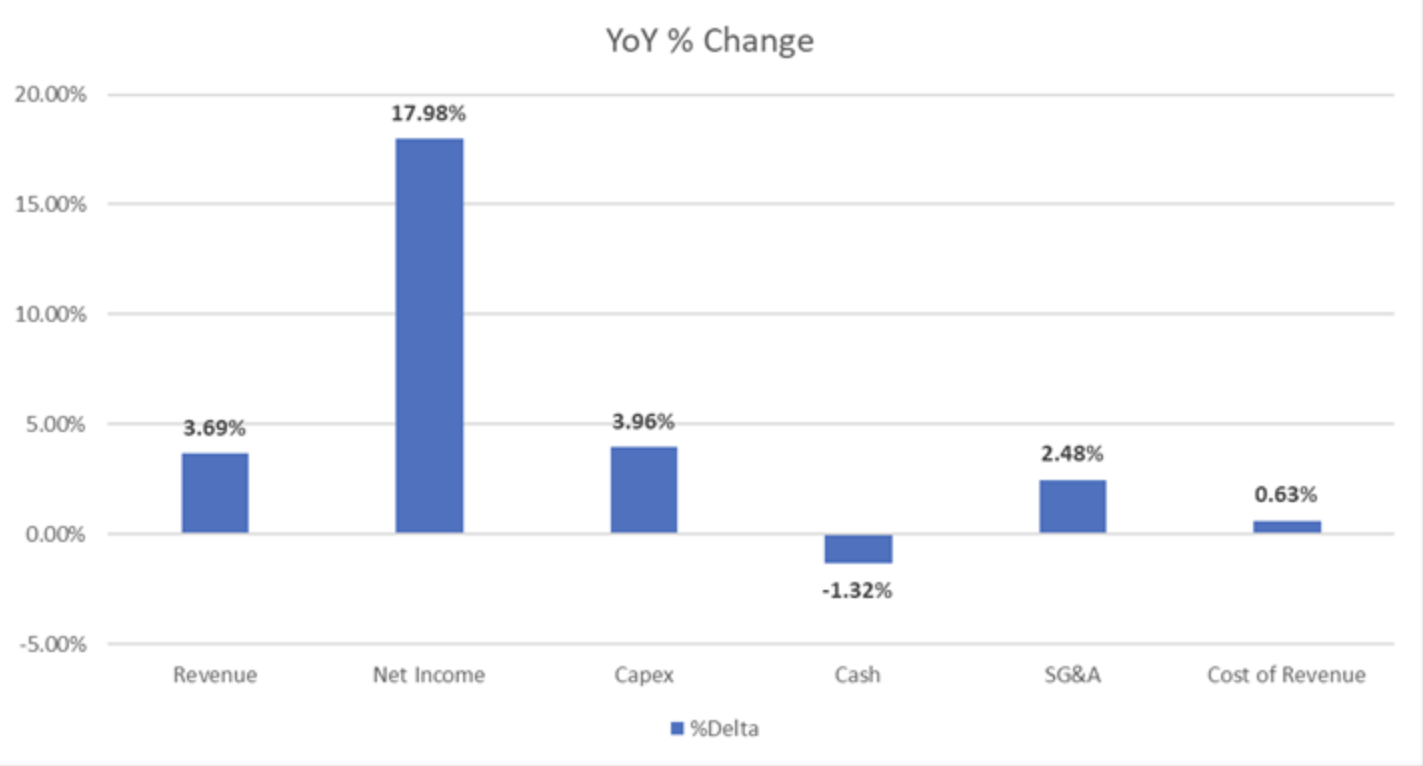

That’s it, folks — the Calcbench Earnings Tracker is calling time today on Q4 earnings, and the past week’s filers delivered a final pop to overall earnings compared to the year-ago period. Our latest analysis captures data from more than 2,100 non-financial firms that had filed Q4 earnings releases by 3 p.m. ET on Friday, Feb. 28. Net income grew nearly 18 percent from the year-ago period, with revenue, capex spending, and Sales, General & Administrative costs all also a few points higher than they were for Q4 2023. Figure 1, below, gives our final numbers for the quarter. Some people might ask, “What about Nvidia? Didn’t they just report gobs and gobs of net income, and is that skewing net income growth for the whole?” That’s a fair question; NVidia ($NVDA) did report $9.8 billion in net income earlier this week, which is indeed an enormous sum. Still, the answer is no, Nvidia’s performance did not skew results to any unusual degree. Even if you exclude the AI chipmak...