Calculating Tax Benefits From the Megabill

So Congress signed the One Big Beautiful Bill into law. Other people can debate the merits of the massive tax and spending plan as a whole — but there’s one implication for corporate earnings that Calcbench can address right away.

The implication is this: the law includes a provision that will allow companies to deduct more of interest expenses they incur from taxable corporate income, which in turn will goose earnings per share upward. And while the deduction is structured in a way that’s likely to be particularly helpful to small companies, Calcbench has developed a template so that financial analysts can quickly estimate the benefit for any public filer.

Under pre-existing tax rules, companies were allowed to deduct interest expense for interest that was as much as 30 percent — but not more — of earnings before interest and tax, otherwise known as EBIT. The One Big Beautiful Bill, however, says that deduction can now equal 30 percent of EBIT plus depreciation and amortization, commonly known as EBITDA.

EBITDA is always going to be larger than EBIT, so therefore the total possible tax deduction is going to be larger too. Which means a larger uplift to corporate earnings.

This newly expanded deduction can boost the earnings of any company, although smaller firms are likely to benefit more because they tend to have relatively larger amounts of depreciation and amortization than their large-cap brethren. That is, EBITDA isn’t just larger than EBIT for small firms; it tends to be considerably larger, so more interest expense is eligible for the new tax credit. (Barron’s has an article taking a deep dive into the issue if you want more detail.)

Anyway, back to our template. Calcbench premium subscribers can download the template from DropBox and then enter the ticker of companies you follow to see whether that company can benefit from this new tax benefit. (The template will only work if you are a premium subscriber and use our Excel Add-In. If you need help with either of those, let us know at us@calcbench.com.)

For example, Figure 1 below shows the results for Fidelity National Information Services ($FIS). Its EBIT for 2024 was $790 million, but its EBITDA was nearly $2.53 billion. That means its interest expense goes from 52 percent of EBIT to 16 percent of EBITDA — therefore yes, it stands to benefit from this new deduction.

Now let’s get to the good stuff: Which companies might stand to benefit the most from this deduction?

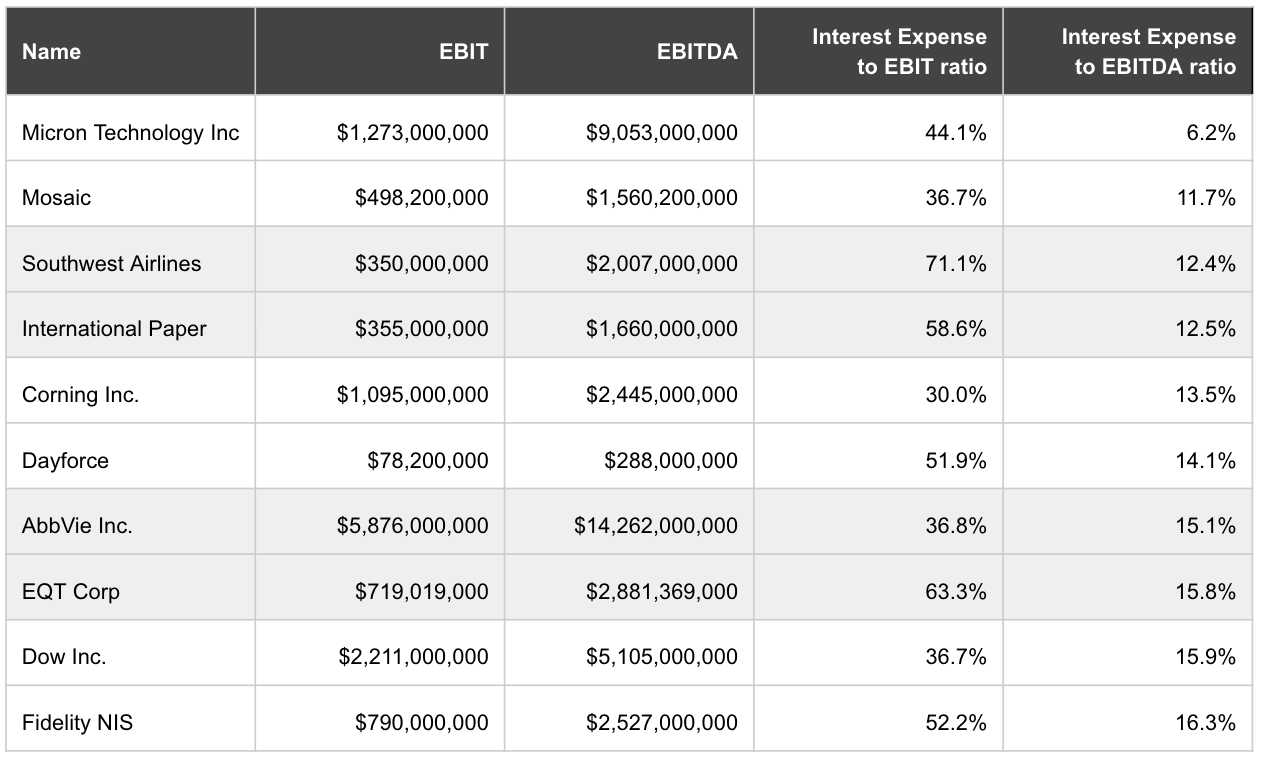

We sifted through S&P 500 firms, looking for non-financial companies with large depreciation and amortization costs, and found several dozen who would see their interest expense ratio decline sharply once you add the DA to the EBIT. Figure 2, below, shows the 10 firms with the largest impact to interest expense and therefore to the EBITDA ratio.

So these 10 firms (plus many more) would now be able to claim a larger tax deduction thanks to the One Big Beautiful Bill, which in turn will help to improve earnings.

You can use our template to research other companies and how they’ll benefit, too. It’s all there in the data, and Calcbench brings it to you.

Comments

Post a Comment