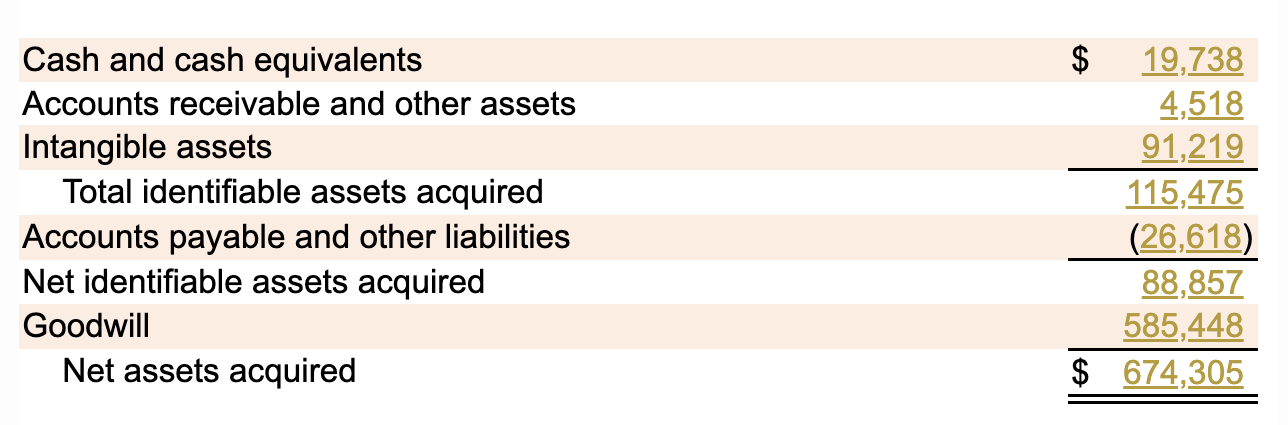

The Details of Software Acquisition Deals

Here at Calcbench we love talking about intangible assets and all the footnote disclosures that exist to help an analyst understand why those assets have the values they do. Today let’s explore those disclosures specifically as they relate to the software sector, since intangibles can often be a huge part of a software company’s total worth. Inspiration for this post came from payments processor Bill.com ($BILL), which filed its latest annual report last week. We were snooping around the company’s business acquisition footnote , and found a discussion of Bill.com’s acquisition of Invoice2Go back in 2021. The deal was valued at $674.3 million, and that purchase price was allocated as follows in Figure 1, below. As you can see, intangible assets were valued at $91.22 million, or 13.5 percent of the total $674.3 million price. (Goodwill was a whopping 86.8 percent of the total price, but we’ve written about goodwill in acquisitions plenty of times before.) So exactly what went into...