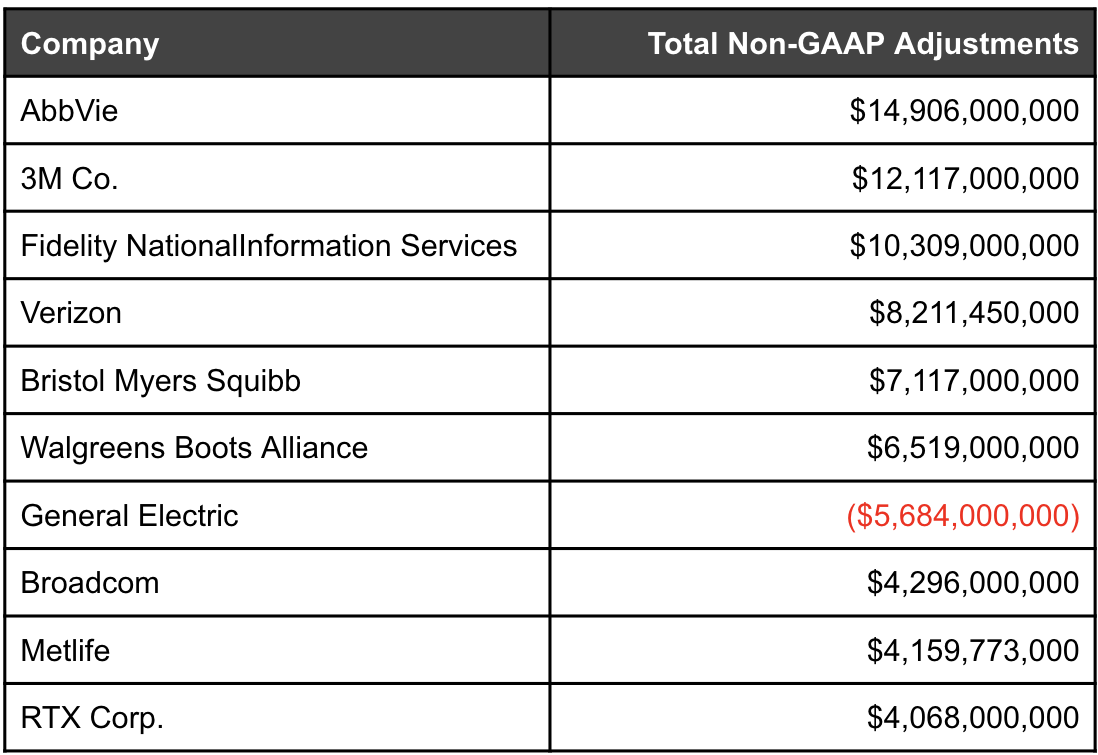

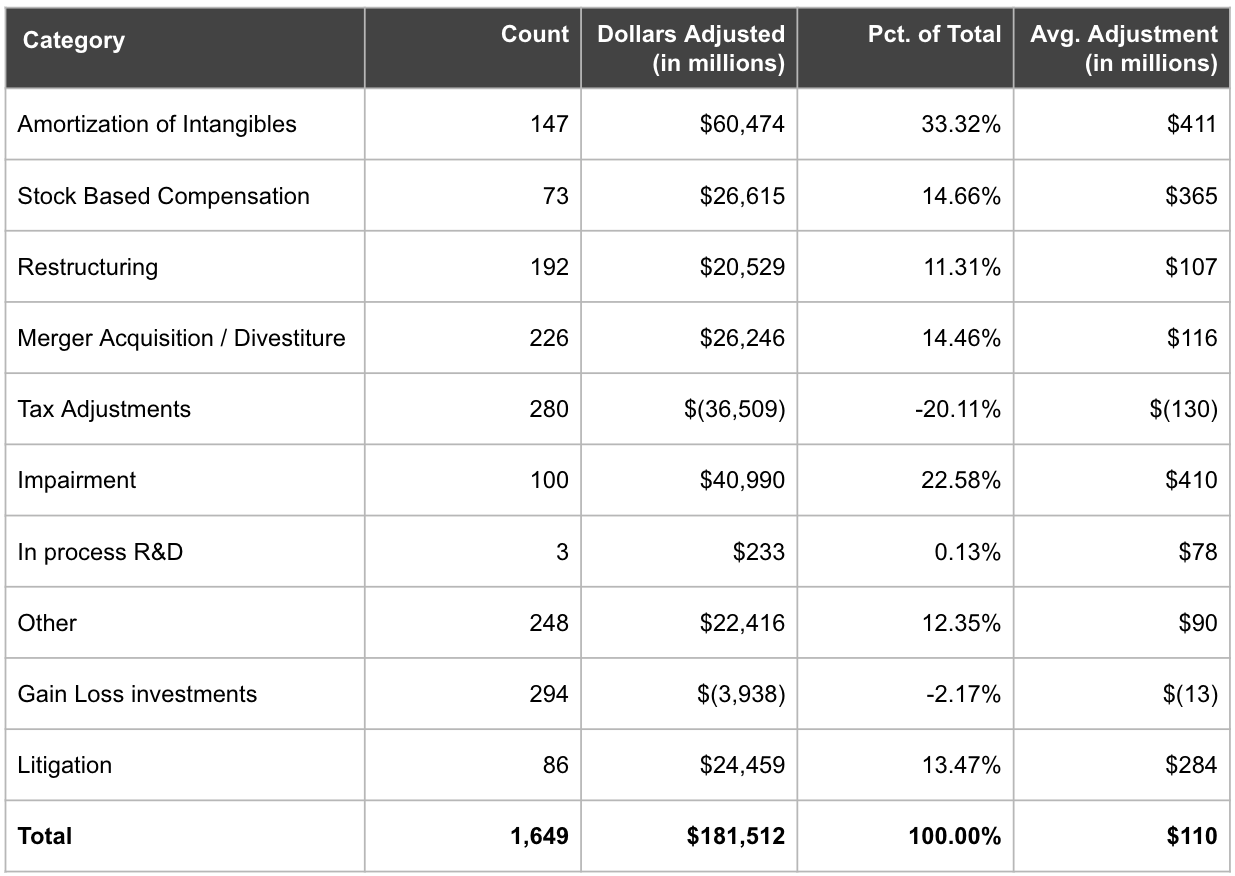

Amortization of Intangibles and Non-GAAP Net Income

As you might have seen, last week Calcbench published our annual analysis of non-GAAP adjustments to net income — and as usual, amortization of intangible assets accounted for a significant portion of all non-GAAP adjustments. Specifically, among the 260 randomly selected S&P 500 firms that we studied, we identified 147 adjustments related to amortization of intangible assets, worth a total of $60.5 billion. That was the largest single category of non-GAAP adjustment by far, roughly one-third of the whole $181.5 billion in non-GAAP adjustments to net income that we identified. Moreover, amortization of intangibles has been one of the largest categories of non-GAAP adjustments for three years running. Even in 2022, when goodwill impairments were the single largest category of adjustment, amortization of intangibles still placed a strong second. Now that inflation and impairments are behind us, amortization is back on top as usual. We should pause to understand why that is. Fir...